The Budget: key points for small business owners

Budget 2025 aims to get the UK economy back on track. But what will the Chancellor’s announcements mean for your small business? We have the Budget lowdown.

The Chancellor of the Exchequer, Rachel Reeves, delivered the Labour government’s Budget on 26 November 2025, with the key aim of bringing the UK economy back under control.

Let’s take a look at the main points from the Budget announcements and how they may affect your small business in the coming months and years.

Budget 2025: the important takeaways for small businesses

The Chancellor presented Budget 2025 as a plan to restore stability and fund public services without raising the main rates of income tax, National Insurance (NI) or VAT. In practice, the OBR estimates that the package will raise about £26 billion a year in extra tax by 2029–30, taking the overall tax burden to a new post-war high.

The economic backdrop is mixed. The OBR now expects the economy to grow by around 1.5% in 2025, slightly faster than it had forecast in March, but with weaker growth further out. Inflation is expected to average about 3.5% in 2025 and 2.5% in 2026 before returning to the 2% target in 2027.

Borrowing is forecast to fall each year over the next Parliament, although public debt as a share of GDP remains close to its recent highs.

Have taxes gone up, as predicted?

For individuals and owner-managed businesses, the key point is that there are no headline increases in the main income tax or corporation tax rates.

Instead, most of the extra revenue comes from freezing thresholds, increasing rates on investment and rental income, and new or extended charges on wealth and assets.

Labour has stuck to its manifesto promise of not raising income tax, NI or VAT. But there are some tax rises and changes to consider.

Frozen income tax thresholds extended to 2031

The existing freeze in the personal allowance and higher rate threshold is being extended by a further three years beyond 2028, so the main income tax thresholds will now remain fixed until April 2031.

The OBR estimates that this ‘fiscal drag’ will bring hundreds of thousands more people into basic, higher and additional rate tax bands over the forecast period, and is one of the single largest revenue raisers in the Budget.

In practical terms, if salaries continue to rise with inflation, more of each pay rise will be taxed, and more people will move into higher rate bands – even if their real standard of living does not improve. For company directors who pay themselves through a mix of salary and dividends, this makes it even more important to review remuneration structures on a regular basis.

Higher tax on dividends, savings and rental income

Income tax rates on dividends, savings income and property income are generally being increased by 2 percentage points. For dividends, the basic and higher rates will rise to 10.75% and 35.75% from April 2026, with the additional rate being unchanged at 39.35%.

For property and savings income, the basic, higher and additional rates will also rise by 2 points from April 2027, taking the rates on both property and savings income to 22%, 42% and 47%.

For many small company owners who extract profits mainly as dividends, and for landlords with personally-held property, this is a significant ongoing cost. It will be important to revisit profit extraction strategies, use of ISAs and pensions, and the split of income between spouses where that’s relevant.

National Insurance on salary-sacrificed pension contributions

From April 2029, salary-sacrificed pension contributions above an annual threshold of £2,000 will no longer be exempt from National Insurance. Contributions above this level will be subject to both employer and employee NIC, at 15% and 8% respectively on earnings within the main band, with the higher 2% employee rate applying above the higher rate threshold.

This change is aimed primarily at higher earners and larger employers that have used salary sacrifice to save NICs on substantial pension contributions. It will reduce the attractiveness of salary sacrifice for directors who currently route large pension payments this way, and may tilt the balance back towards more conventional dividend and bonus planning in some cases.

High-value council tax surcharge (aka the ‘mansion tax’)

From April 2028, owners of residential properties in England worth more than £2 million will pay a new ‘high value council tax surcharge’. The surcharge will be banded, starting at £2,500 a year for properties valued between £2 million and £2.5 million, rising to £7,500 for properties over £5 million, payable in addition to normal council tax.

The Government expects this to affect fewer than 1% of properties. A scheme will be developed to allow payment to be deferred until the property is sold or the owner dies.

Electric and plug-in vehicle mileage tax

From 2028/29, a new mileage-based charge will apply to battery electric and plug-in hybrid cars. The initial rates will be 3p per mile for fully electric vehicles and 1.5p per mile for plug-in hybrids, with rates increasing with inflation each year.

This is expected to raise around £1.4 billion once fully implemented.

The detail of how this will interact with existing rules for business mileage claims and advisory rates is not yet clear. For now, the message is that the tax advantage of running an electric vehicle is being reduced over time, even though company car benefit charges remain significantly lower than for conventional cars.

Corporation tax relief on capital investment

The main writing-down allowance rate for plant and machinery that’s not covered by full expensing or the Annual Investment Allowance (AIA) will be cut from 18% to 14% from April 2026. This slows the rate at which companies can obtain tax relief on qualifying expenditure that sits in the main pool.

For many small companies that keep capital spend within the £1 million AIA limit, this change will have limited impact. It will, however, matter for larger investments that fall outside the AIA or full expensing rules, and for unincorporated businesses where similar rates may apply for income tax purposes. The overall direction of travel is still towards more generous up-front relief but less generous ongoing relief.

Employee ownership trusts

Capital gains tax relief on disposals of businesses to employee ownership trusts (EOTs) will be reduced from 100% to 50%. This means that half of the qualifying gain will become subject to CGT at the appropriate rate, with detailed rules still to be confirmed.

EOTs will remain an attractive route in some situations, particularly where succession and employee engagement are priorities, but the tax advantage is now less generous. Anyone contemplating an EOT sale will need careful modelling of after-tax proceeds compared with a conventional share sale.

Business rates and sector-specific measures

Business rates will be reduced for around 750,000 retail, hospitality and leisure properties, funded by higher rates on larger premises and warehouses such as those used by online retailers.

There are also targeted measures such as a new tax on ride-hailing journeys (for example Uber and Bolt) and an extension of the soft drinks levy to a wider range of high-sugar drinks. For many bricks-and-mortar businesses this should provide some modest relief on property costs, although it will take time for the detail to filter through to actual bills.

Homeworking expenses relief withdrawn

From 6 April 2026, employees will no longer be able to claim income tax relief for additional household costs when they’re required to work from home and their employer does not reimburse those costs.

This removes both the flat £6 per week homeworking easement and claims based on actual extra costs. Employers will still be able to reimburse eligible homeworking expenses without deducting tax or National Insurance.

Other points to note

Among the many Budget announcements there were several other changes that it’s important to have on your radar as a small business owner.

a) ISA savings: From April 2027, the overall £20,000 ISA limit stays the same, but new cash ISA subscriptions will be limited to £12,000 a year (£20,000 still allowed for those aged 65+). The rest of the allowance can be used for any other type of ISA.

b) Fuel duty: Fuel duty is frozen until September 2026, with the temporary 5p cut also extended to that date. Staged increases are planned thereafter.

c) Welfare changes: The two-child benefit cap will be removed from April 2026 and working-age benefits will be uprated in line with inflation.

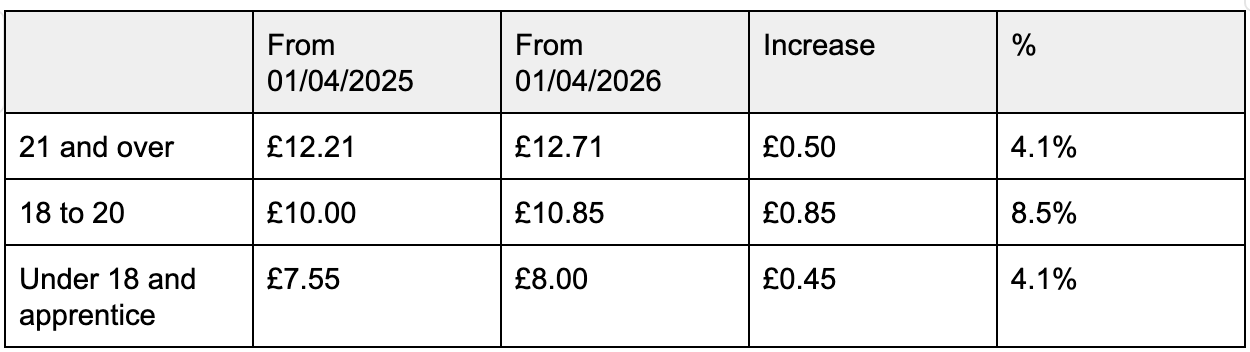

d) National Living Wage: The National Living Wage will increase again from April 2026, adding to wage costs in labour-intensive sectors:

e) Gambling, tourist and other specific taxes: There are increases to the taxation of remote gambling, a new tourist tax on overnight stays, and various other targeted measures that may affect particular clients such as hoteliers or leisure businesses.

Overview

Overall, the Budget continues the pattern of raising revenue by tightening the tax treatment of wealth, investment and property, while relying on frozen thresholds to increase the effective tax take on earned income over time.

For many small business owners the headline tax rates may look unchanged, but the cumulative effect of these measures over the rest of the Parliament will be significant.

If you’re concerned about any of the announcements made in Budget 2025, come and talk to our team. We’ll be happy to run through the shorter and longer-term implications of these changes and what they will mean for your business in 2026 and beyond.

If you’re concerned about any of the announcements made in Budget 2025, come and talk to our team. We’ll be happy to run through the shorter and longer-term implications of these changes and what they will mean for your business in 2026 and beyond.

Get in touchRelated Articles

Keeping you up to date with the latest Statutory Sick Pay rules

From 6 April 2026, the rules around Statutory Sick Pay (SSP) changed. We highlight the key changes and the potential impact on your payroll system.

Read On

Getting ready for Making Tax Digital for Income Tax

MTD for Income Tax starts April 2026—check if you’re compliant and how to prepare as a sole trader or landlord.

Read On

5 major challenges for the manufacturing sector

Discover 5 key Industry 4.0 challenges for modern manufacturers and how to update your strategy to stay competitive.

Read On